August 12, 2022

The United States Senate voted to pass the Inflation Reduction Act, 51-50, with Vice President Kamala Harris breaking the tie. Late last week, Senator Kyrsten Sinema (D-AZ) announced her support for the package negotiated by Senate Majority Leader Chuck Schumer (D-NY) and Senator Joe Manchin (D-WV) after securing changes to the tax provisions, which included changes to the book minimum tax, removal of carried interest provisions, and the addition of the stock buyback provisions. The book minimum tax changes included an exemption for the accelerated depreciation of some capital expenditures, a change that domestic manufacturers strongly supported.

Prior to the Senate debate, the Senate parliamentarian completed the “Byrd Bath” and ruled most of the bill in order. The exception was her ruling that the provision that would have required drug companies to pay rebates to the Department of Health and Human Services (HHS) if prices for drugs were raised more than the rate of inflation for individuals with private health insurance was out of order.

As anticipated, Republicans offered over roughly 520 amendments, coupled with a small number of amendments offered by Senate Democrats to reach a total of 547 amendments to the substitute amendment. Ultimately, only 37 amendments and points of order received a floor vote and only two were adopted.

House Democratic leadership instructed members to plan for a Friday morning vote; which was passed along party lines by a vote of 220-207.

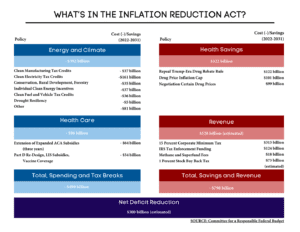

The initial package was projected by the Congressional Budget Office (CBO) to reduce deficits by $300 billion over the next 10 years. However, with the recent changes to the tax provisions, the parliamentarian review, and the adopted amendments, the CBO had to re-review the package. The CBO estimates that the Ways & Means tax provisions would reduce deficits by over $1 billion over the next decade, while increasing Energy and Commerce provisions by roughly $487 billion, Agriculture provisions by $89 billion, Natural Resources provisions by roughly $26 billion, Science, Space, and Technology provisions by $45 billion, Transportation provisions by $60 billion, Oversight and Reform provisions by roughly $8 billion and Homeland Security provisions by $500 million until 2031. Below are details of the amendments and the overall package.

Tax Provisions

Stock Buyback Tax

The bill will levee a 1 percent excise tax on stock buybacks. This provision is expected to raise $74 over the next decade. The tax will impact the largest companies that utilize buybacks as a means to increase stock prices.

Corporate Taxes

The bill imposes a 15 percent corporate alternative minimum tax (AMT), commonly referred to as the “book minimum tax,” on companies that have traditionally been able to pay little-to-no taxes due to credits and/or deductions. The book minimum tax is typically applied to a company’s “book” or financial statement earnings, rather than the traditional income calculation used for tax purposes. Corporations will be allowed to claim tax credits and depreciation tax deductions against the AMT and be eligible to claim a tax credit against the regular corporate tax for AMT paid in prior years, to the extent the regular tax liability in any year exceeds 15 percent of the corporation’s adjusted financial statement income. As currently proposed, this bill would leave much of the Tax Cuts and Jobs Act (TCJA) in effect, including keeping the 21 percent corporate rate. Also, due to the changes from the adopted amendments, language includes a carve out for private equity, which that means fewer companies owned by investment firms will have to pay the tax. This provision will likely raise slightly less than $313 billion.

IRS Enforcement

The bill would allocate additional money to the Internal Revenue Service (IRS) to add auditors, improve customer service, and modernize technology. The bill would invest $80 billion over the next 10 years to increase tax revenue by $203 billion through a crackdown on individuals cheating on their taxes and strengthening the power of the IRS. The IRS funding includes funding for taxpayer services, enforcement, operations support, and business systems modernization. This provision raises approximately $124 billion.

Climate Change/Clean Energy

The bill proposes investing $369 billion in energy security and climate change programs over the course of the next 10 years. The key components of the energy provisions aim to lower energy costs in the United States; increase American energy security; invest in decarbonizing all sectors of the economy via innovative solutions; invest in disadvantaged communities; and support resilient rural communities.

Lower Consumer Energy Costs

The bill proposes direct consumer incentives to buy energy efficient and electric appliances, clean vehicles, and rooftop-solar, and invest in home energy efficiency, with a significant portion of the funding going to lower income households and disadvantaged communities. This includes: $9 billion for consumer home energy rebate programs; 10 years of consumer tax credits for energy efficient homes and for clean energy; $4,000 consumer tax credit for lower/middle income to purchase used electric vehicles (EVs), and up to $7,500 tax credits for new clean energy vehicles; and $1 billion grant program for energy efficient affordable housing.

Energy Security and Domestic Manufacturing

The bill includes investments of over $60 billion to onshore clean energy manufacturing, and incentives to reduce inflation and the risk of future price shocks by bringing down the cost of clean energy and clean vehicles and relieving supply chain bottlenecks. The investments include $10 billion investment tax credit to build clean technology manufacturing facilities; $500 million for the Defense production Act for heat pumps and critical minerals; $2 billion in grants for auto manufacturers; $20 billion in loans for new clean vehicle manufacturing; and $2 billion for National Labs for energy research purposes.

Decarbonize the Economy

The bill would invest in reduction of carbon emissions via tax credits for clean energy sources; $30 billion in targeted grant and loan programs; tax credits for clean fuels and commercial vehicles; grants and tax credits to reduce emissions, including $6 billion for a new Advanced Industrial Facilities Deployment Program; over $9 billion for Federal procurement; $27 billion for clean energy technology accelerator; and a Methane Emissions Reduction Program.

Environmental Justice

The bill includes over $60 billion for environmental justice programs including: Environmental and Climate Justice Block Grants; Neighborhood Access and Equity Grants; Ports Air Pollution Reduction Grants; $1 billion for clean heavy-duty vehicles; and additional programs focused on disadvantaged and low-income communities. This includes roughly $3 billion for environmental justice block grants, such as $20 million for technical assistance at the community level. Additionally, the bill allocates over $3 billion for air pollution monitoring in low-income communities. Also, the bill permanently extends and increases the Black Lung Disability Trust Fund, which is a tax on coal production to finance workers’ claims.

Rural Communities

The bill would make investments in rural communities including over $20 billion to support climate smart agriculture practices; $5 billion in grants to support forest resiliency programs, conservation, and urban tree planting; tax credits to build infrastructure for sustainable aviation fuel and other biofuels; and $2.6 billion in grants for conservation and restoration of coastal habitats.

Electric Vehicles

Provisions aim to boost electric vehicle makers and green energy companies. The bill includes provisions for a $4,000 tax credit for lower and middle-income buyers for the purchasing of used EVs, and up to $7,500 tax credit for new EVs.

Energy Investment

Invests in the technologies needed for all fuel types, including hydrogen, nuclear, renewables, fossil fuels, and energy storage, to be produced and used in the cleanest way possible.

Fossil Fuels

This bill does not arbitrarily shut off America’s abundant fossil fuels and invests heavily in technologies to help the U.S. reduce its domestic methane and carbon.

Drought and Water Security

The bill includes $4 billion for drought relief to help Western states at risk of low water levels. The funds are to be utilized by these states for the purchase private water rights and to provide municipalities assistance with conservation projects to increase water levels in the Colorado River system.

Public Lands

The bill includes language for a minimum royalties increase for companies to pay the federal government for oil and gas extraction on public lands and waters. Also, the bill ties requirements for solar and wind to lease sales that open up new oil and gas production.

Other Energy Provisions

The bill includes a tax credit that expands energy efficiency in commercial buildings. Additionally, the bill includes a new program aimed to reduce emissions from oil and gas, by providing grants and loans for companies reining in their emissions, and imposing fees on producers with excess methane emissions. Also, $27 billion would go towards a green bank to provide incentives for clean energy technology.

Health Care

The bill includes a significant set of drug pricing reforms and an extension of higher subsidies for purchasing commercial insurance in the federal marketplace. The drug pricing reforms collectively represent a significant source of revenue for the bill through savings to the federal government, while the subsidies represent an expenditure.

Negotiation

The bill removes the non-interference clause that prevents HHS from negotiating with manufacturers and establishes a scheme for the Secretary to negotiate the price of a limited set of drugs provided through Medicare Parts B and D each year, while setting parameters for the range of acceptable prices. The bill specifies the number of drugs subject to negotiation each year and also limits the drugs that would be eligible for negotiation to those without competition.

Inflationary Rebates

The bill would require drug manufacturers who increase drug prices over the rate of inflation in Medicare Parts B and D to pay the difference in a rebate to HHS each year.

Medicare Part D Reforms

Medicare provides prescription drug benefits to beneficiaries through Medicare Part D, under which Medicare contracts with commercial health plans to administer the benefit. Liability for costs of the drugs shifts over the course of the benefit between beneficiaries, Part D plans, and manufacturers. The bill limits beneficiary out-of-pocket costs to a lower amount and shifts greater liability to plans and drug manufacturers in different phases of the benefit. The bill also broadens eligibility for the Low-Income Subsidy, a program for beneficiaries in Part D under which Medicare pays for a significant portion of the beneficiary’s premiums and out-of-pocket costs. Finally, the bill waives beneficiary cost sharing for vaccines covered under Medicare Part D (which does not include COVID-19 or flu vaccines, which are covered under Medicare Part B).

Insurance Subsidies

The Affordable Care Act established federal subsidies for consumers within a particular income range (133 – 400 percent of the Federal Poverty Level) that purchase insurance through the federal marketplace. The American Rescue Plan Act included a temporary but significant increase in the level of the subsidies available for consumers and also waived the 400 percent FPL income cap. Those temporary provisions expire at the end of 2022. The bill would extend those provisions through 2025.

Insulin

The bill will cap the price consumers in Medicare pay for insulin to $35 starting in plan year 2023.

Adopted Amendments

Thune amendment (5472):

Senator John Thune (R-SD) submitted an amendment to narrow the scope of corporation minimum tax provisions and to provide an extension on State and Local Tax (SALT) deductions. Specifically, the amendment made changes to the provisions related to depreciation tax deductions against the AMT. This amendment removed provisions that would require subsidiary businesses of any size held by funds or partnerships to combine unrelated income that determines corporation status of an aggregate $1 billion income threshold. The language prior to this amendment would have directly impacted small to mid-size businesses and had been projected to raise $35 billion. To balance the scoring of the amendment, 5472 also extended SALT deduction caps for an additional year until 2027.

Warner amendment (5488):

Senator Mark Warner (D-VA) offered an amendment that extends pass-through loss limitations for an additional two years and revised the Thune amendment by reinstating the SALT deduction effective dating back to 2026.